STRATIQ

Quick Start — How to export your strategy from TradingView

1

Open Strategy Tester in TradingView

Go to your chart → attach your Pine Script strategy → open the Strategy Tester panel at the bottom of the screen.

2

Download .XLSX export

Strategy Tester → Performance Summary → click the download icon (↓) → “Save as .xlsx”.

3

Drop the file into Stratiq

Drag & drop your .xlsx into the upload zone below — or click “Add files”. Everything runs locally. Zero bytes uploaded.

DASHBOARD

DASHBOARD

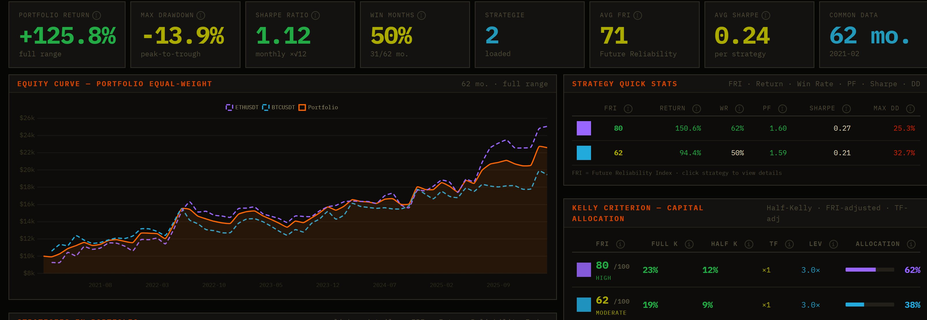

Step 2 — Your strategy, decoded

Stratiq instantly turns your .xlsx into a full portfolio dashboard.

Drop a second strategy to unlock cross-strategy diversification analysis.

- Portfolio metrics — Return, Max Drawdown, Sharpe Ratio, Win Months & equity curve

- FRI scoring — Future Reliability Index: OOS validation, walk-forward consistency, PF stability

- Kelly position sizing — FRI-adjusted Half-Kelly allocation with leverage caps per asset class

- Monte Carlo forecasts — 1,000 simulations, percentile bands P10–P90, stress tests on historical crises

- Correlation matrix — Find strategy pairs that hedge each other & avoid simultaneous drawdowns